About

Strategies

Strategies

Track Record

Insights

Insights

Investor Guide

Education

Blog & Articles

FAQ

Investor Resources Hub

Curated insights for smarter investing.

Additional

Careers

Team

Contact our Team

Newsletter-Sign Up

English

Spanish

Request Access

Request Access

Client Login

Client Login

Request Access

Request Access

Client Login

Client Login

News and insight from the

Infinity

9

team

Insight

October 8, 2025

How Institutional Investors Think (and How to Apply It to Your Personal Portfolio)

Read article

Read article

All

Insight

News

How Institutional Investors Think (and How to Apply It to Your Personal Portfolio)

Insight

October 8, 2025

The New Latino Elite Invests Without Fear: How a Mindset Shift Is Creating a Generation That Transcends

Insight

October 1, 2025

CIO Market Update Q3 2025

Insight

October 1, 2025

Why Saving in Local Currency Is Like Storing Water in a Strainer

Insight

September 24, 2025

What Most Operators Won’t Tell You (But You Should Ask Anyway)

Insight

September 10, 2025

The "Sleep Well" Portfolio: What Calm, Confident Investors Focus on in Real Estate

Insight

September 8, 2025

Do You Want Control or Simplicity? The Real Tradeoff in Passive Investing

Insight

September 5, 2025

What Happens If You Don’t Plan Ahead: Cross-Border Estate Planning Mistakes to Avoid

Insight

September 3, 2025

How Family Offices Underwrite Sponsors—and What You Can Learn from Them

Insight

September 1, 2025

Understanding Real Estate Cycles as a Foreign Investor: When to Act and When to Wait

Insight

August 29, 2025

What ‘Skin in the Game’ Really Means—and Why It Matters to You

Insight

August 27, 2025

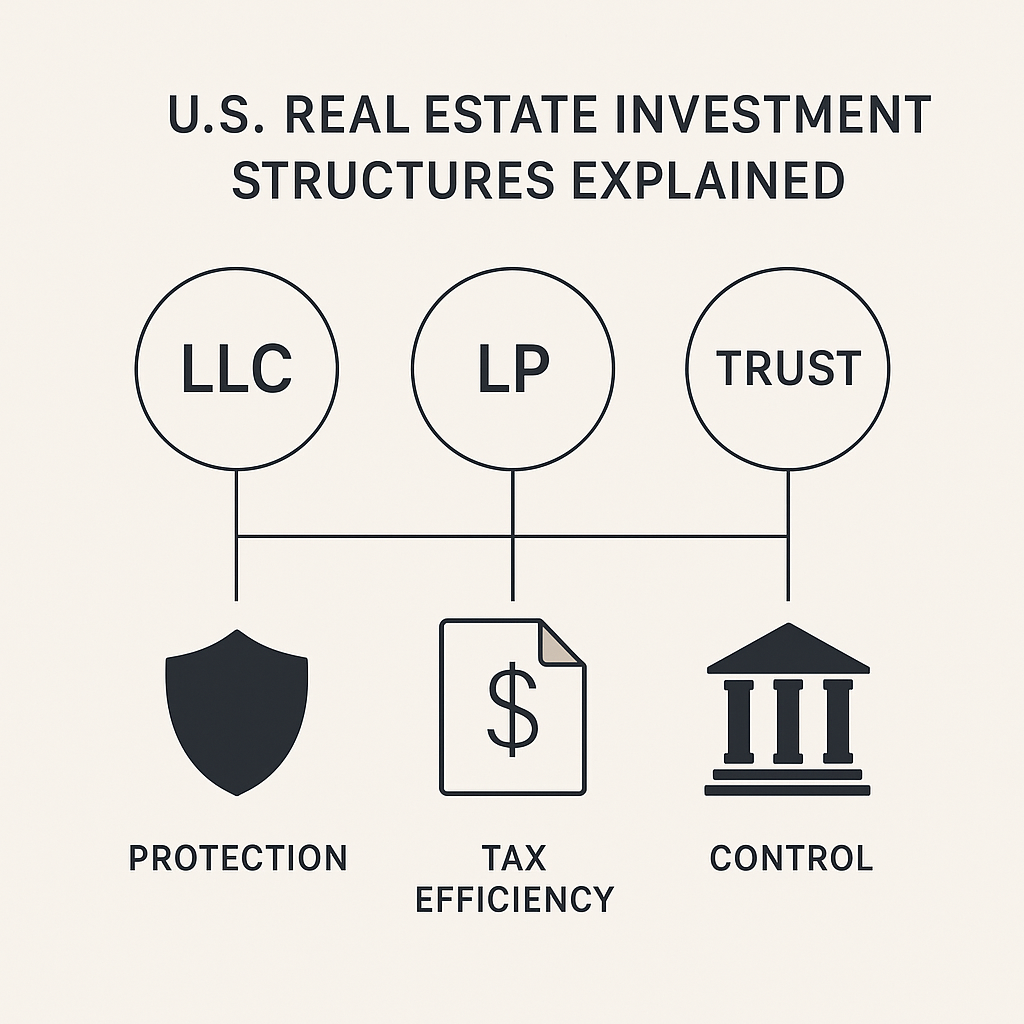

U.S. Real Estate Investment Structures Explained (LLC vs. LP vs. Trust)

Insight

August 25, 2025

How to Read an Investment Deck: What to Look for Beyond the IRR

Insight

August 22, 2025

Is Your Capital Safe in the U.S.? Understanding Legal Protections for Foreign Investors

Insight

August 20, 2025

The Step-by-Step Guide to Investing in U.S. Real Estate from Latin America

Insight

August 18, 2025

What ‘Skin in the Game’ Really Means in Investing—and Why It Matters to You

Insight

August 15, 2025

U.S. Real Estate Investment Structures Explained: LLC vs. LP vs. Trust

Insight

August 11, 2025

How to Read an Investment Deck: What to Look for Beyond the IRR

Insight

August 8, 2025

How to Evaluate a Real Estate Operator Like a Family Office Would

Insight

August 6, 2025

Inside the Term Sheet: What to Ask Before You Wire a Dollar into a Real Estate Deal

Insight

August 1, 2025

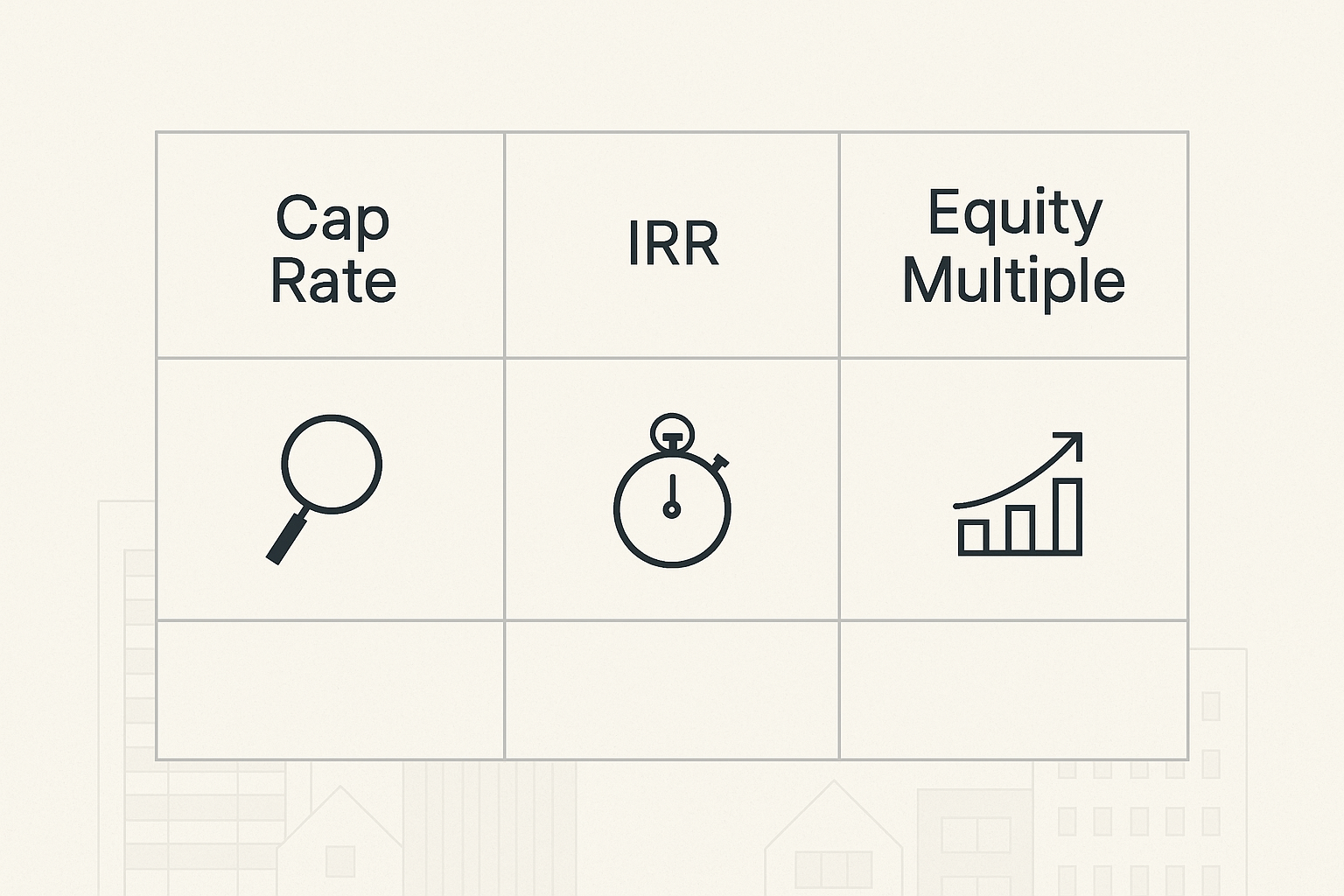

Cap Rate vs. IRR vs. Equity Multiple: What Passive Investors Really Need to Know

Insight

July 30, 2025

Can You Really Trust a U.S. Sponsor? What Global Investors Must Know Before Investing Abroad

Insight

July 25, 2025

Cross-Border Pitfalls: 5 Mistakes Latin American Investors Make When Buying in the U.S

Insight

July 23, 2025

Investing From Abroad: What Latin Americans Need to Know Before Entering the U.S. Market

Insight

July 21, 2025

Why Liquidity Isn’t Always Your Friend: Lessons in Long-Term Wealth Building

Insight

July 18, 2025

The 3 Traits of Investors Who Build Generational Wealth (And How to Cultivate Them)

Insight

July 16, 2025

How Smart Investors Build U.S. Real Estate Portfolios Without Managing Properties

Insight

July 14, 2025

We’re in the News: UAE Stories Shares the Origin of Infinity⁹

News

July 14, 2025

What a Smart Investor Looks Like in 2025 (Hint: It’s Not About the Portfolio Size)

Insight

July 9, 2025

From Public Markets to Private Deals: How New Investors Can Invest Like Institutions

Insight

July 7, 2025

The Global Real Estate Starter Plan: Passive Income, Long-Term Thinking, No Drama

Insight

July 4, 2025

Why Most First-Time Investors Chase the Wrong Metrics in Real Estate

Insight

July 2, 2025

Real Estate Without Borders: What Latin American Investors Should Know in 2025

Insight

June 30, 2025

Why Private Real Estate Is a Smarter First Investment Than REITs or Mutual Funds

Insight

June 30, 2025

The Capital Framework for New Investors: Build Wealth with Strategy, Not Luck

Insight

June 27, 2025

Should You Buy a Rental Property in 2025? What First-Time Investors Need to Know

Insight

June 25, 2025

From Curiosity to Capital: How First-Time Investors Can Confidently Enter Real Estate

Insight

June 20, 2025

Real Estate Investing for Beginners: What Smart Investors Get Right from Day One

Insight

June 18, 2025

From HNW to Ultra-HNW: How Structured Real Estate Investments Accelerate Wealth Compounding

Insight

June 13, 2025

Case Study: How Structured Debt Helped Investors Thrive During Economic Uncertainty

Insight

June 9, 2025

Institutional vs. Entrepreneurial Investing: Why the Smartest Investors Blend Both

Insight

June 6, 2025

How Cross-Border Investors Can Legally Reduce U.S. Estate Tax Exposure Through Proper Real Estate Structuring

Insight

June 2, 2025

Why Investors Should Choose a U.S. Private Real Estate Investment Manager Over a Broker

Insight

May 30, 2025

U.S. Tax Strategies for Latin American Real Estate Investors: What You Should Know (Without Giving Tax Advice)

Insight

May 29, 2025

Most People Buy Real Estate. Smart Investors Allocate Capital.

Insight

May 23, 2025

Preferred Equity Unveiled: How Family Offices Use Structured Investments to Control Risk

Insight

May 7, 2025

The Psychology of Elite Investors: Avoiding Emotional Pitfalls in Real Estate Investing

Insight

May 7, 2025

Volatility-Proof Portfolios: Real Estate Strategies That Outperform in Any Market

Insight

May 7, 2025

Protecting Wealth Across Borders: How Smart Family Offices Diversify Internationally

Insight

May 7, 2025

Why Structured Real Estate Investments Are the New Safe Haven for International Investors

Insight

May 6, 2025

Why Most Investors Misunderstand Real Estate Risk—And How to Get It Right

Insight

Cycle Savvy: Why Timing the Real Estate Market Doesn’t Work and What Smart Investors Do Instead

Insight

Charting a Path to Success: Ahmad Ashrafi and Infinity⁹ Featured in VCPost

News

Infinity⁹ Announces Strategic Investment in Whole Foods-Anchored Shopping Center in Boynton Beach

News

Unlocking Potential: Ahmad Ashrafi Leads Infinity9 To Empower Foreign Investors In US Real Estate

News

CEO Ahmad Ashrafi Shares Insights in Forbes Article: “Why Everyone Should Have a Family Office”

News

Navigating Retirement: Insights from Ahmad Ashrafi Featured in Forbes

News

Principles of Success: Ahmad Ashrafi and Infinity⁹ Featured in Haute Living

News

Infinity9 Investment Group Announces a Strategic Co-GP Capital Funding Platform for Investors

News

Infinity Investment Group and A9 Family Office Launch U.S. Real Estate Investment Fund

News